Risk Management: The Best Defense is a Good Offense

Risk management in day trading involves strategies to protect capital and minimize losses while maximizing potential gains. Key techniques include setting stop-loss orders, using position sizing to limit exposure, and diversifying trades to avoid putting too much at risk in any single position. Effective risk management helps traders maintain consistency and avoid significant drawdowns, ensuring long-term survival in the volatile markets.

1/24/20254 min read

Risk Management Strategy Squeezes Profit From Losing Trades

Imagine two traders - Trader Pim and Trader Slim.

Similarities

Both traders have a starting balance of $10,000. Both are trading Dow Jones futures. Both are following the same trading signals.

Differences

Trader Pim trades a fixed position of one contract, which ticks at $5 per point.

Trader Slim uses a 2% risk strategy, so he trades different position sizes on each trade.

The trades were losers but Trader Slim ended the day in profit.

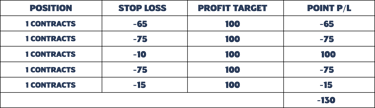

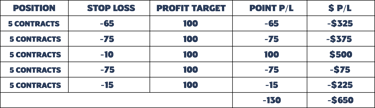

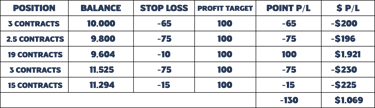

There were a total of five trades - all of which, when combined, ended in a loss of -130 points.

Though Trader Pim ended the day down only -$650, Trader Slim went home with +$1,068 profit.

How was that even possible?

The answer is risk management. It’s not that Trader Slim lost less due to his risk management strategy, it’s that his strategy allowed him to win more.

In short, risk management was not just a defensive strategy but an aggressive one as well. Let’s break it down.

Breaking Down the Trades

The total system loss amounted to -130 points.

The exit rules in this system are simple: close out at the maximum profit target or allow your position to get stopped out (at the stop loss).

Trader Pim’s Losing Strategy

Trading a fixed amount will give a result matching the systems profit loss adjusted for value. In this case, $5 per point. So a loss of -130 points amounts to (-130*5 = -325) a -$650 loss.

Trader Slim’s Aggressive Risk Management Strategy

To come up with 2% risk, multiply the trading account size with 0.02 (account x 2%).

For the max dollar-per-point value, divide max risk by stop loss (e.g. the first trade - $200 divided by 65 = $3.07 value).

Same Win Rate, Different Profit Factor

Win rate is the frequency of wins, often expressed as a percentage. The profit factor is the ratio of wins to losses.

The System:

The system’s win rate for these last five trades was poor - 20% win rate, and 80% losses.

The system’s profit factor was poor 0.43 to 1, or inversely, 2.31 to 1 (loss factor).

Pim’s win rate and profit factor mirrored the system’s, as used a fixed allocation for each trade.

Slim’s win rate was the same as the system’s and the same as Pim’s.

The profit factor surprises with 2.25 to 1. For every one unit lost, a gain of 2.25 units in profit.

To reiterate, the difference between Pim’s loss and Slim’s win is the risk management strategy to guide position sizing. And the difference is night and day.

At What Point Will Win Rate Interfere With Profit Factor and Vice Versa?

Imagine a trading system that had a win rate of only 30% but it made double what it lost. If its average win was $100, it’s average loss was $50, can you expect it to generate positive returns? The answer is no, you can’t.

But what if it made an average of $120 and an average loss of $50. Does it have a positive trading expectancy? Yes, it does.

Let’s play with this idea some more.

Let’s take the first example, wherein a system has an average gain of $100 and an average loss of $50.

At its current 30% win rate, it’s a loser. What if its win rate were 32% instead? It’s still a loser. What if its win rate was slightly higher, at 35%?. In this case, it’s potentially a winner.

How did we just figure this out? Simple, we calculated the trading expectancy.

Introducing Trading Expectancy

Trading expectancy is a calculation you use to theoretically predict the favorability of a trading system - whether winning or losing - based on its win rate and its average wins and losses (almost like profit factor).

Trading expectancy sets a limit at zero. If a system’s trading expectancy is below zero, it’s a loser. If it’s above zero, it’s a potential winner.

(Win % x Average Win) - (Loss % x Average Loss) = Trading Expectancy

Trading Expectancy of a Coin Toss and a Weighted Coin Toss

If the coin shows heads, you win a dollar; tails, you lose a dollar. A 50/50 bet. How might it look in terms of trading expectancy?

Win rate = 50%; Loss rate = 50%

Average win = $1.00; Average loss = -$1.00.

Plug in the numbers: (0.50 x 1) – (0.50 x 1) = 0 trading expectancy. Over time, neither a winning nor a loser. You do, however, lose time and effort.

What if same presented a slight variation - a weighted coin toss:

The coin is weighted so that it tends to land “heads” 75% of the time, returning $1 and a loss of $2.50. A tails win will return $2.50 and a loss of $1.

The winning bet would still be heads, with a trading expectancy of 0.125 not the biggest winner, it’s still the only bet that won’t lose over time.

Using Trading Expectancy to Analyze Trades

System 1 wins only 20% of the time, returns an average of $425, loses an average of $100.

System 2 wins 95% of the time, returns an average of $50, loses an average of $975.

System 3 wins 65% of the time, returns $200 on average, loses $375 on average.

Objectively determine that system 1 is the only winner.

The best defense is a good offense.

The only good defense is to attack.

Let’s transform this: the best “defensive strategy” has an effective “aggressive (offensive) component.”

© 2025. All rights reserved.

You understand and acknowledge that there is a very high degree of risk involved in trading securities and, in particular, in trading forex, futures and options. Please ensure that you fully understand the risks involved. The site is providing educational content which will provide you with an indepth knowledge of the market. This site is in no way providing any investment, financial, tax, or legal advisory and do not purport to provide personalized investment, financial, tax, or legal advice in any form. None of the provided information does recommend the purchase of particular securities, nor does the provider promise or guarantee any particular results. The provider assumes no responsibility or liability for your trading and investment results, and you agree to hold the provider harmless for any such results or losses. It is up to you as a trader to make your own judgement using your own analysis.